Ijraset Journal For Research in Applied Science and Engineering Technology

Investment Portfolio Management System Using Machine Learning

Authors: Payal Narale, Vinay Lachotra, Krushna Nalawade, Sakshi Karanje, Savita Vibhute

DOI Link: https://doi.org/10.22214/ijraset.2024.59541

Certificate: View Certificate

Abstract

Portfolio management is the concept of determining the proportions of various assets to be held in a portfolio in order to maximize return while minimizing risk exposure. Investment banking and financial management both depend heavily on portfolio optimization. Choosing the greatest feasible combinations of several portfolios to construct an optimal portfolio is an exponentially complex challenge in terms of computation. It\'s commonly believed that public opinion and financial markets are intertwined. Recently, a variety of machine learning algorithms have been employed to anticipate short-term financial markets with positive outcomes. On the other hand, historical returns don\'t seem to fit the normal distribution theory. But sentiment analysis performs better when combined with long short-term memory networks and historical data. In this project, we want to use AI/ML to predict portfolio risk and provide insights into how stocks will perform. We will train our model using datasets obtained from the Yahoo Financial API that include historical data from the top 100 companies (NIFTY 100) in the NSE and BSE from 2010 to 2021.

Introduction

I. INTRODUCTION

Artificial intelligence-based machine learning (ML) models are the latest technological innovation to hit the portfolio management industry. And while, at least so far, ML models have not been a panacea for active investment managers, they’ve proven themselves a valuable tool by augmenting human decision-making around important activities such as asset allocation, risk management, and portfolio construction. Investment Portfolio Management is a concept where the risk correlated to the investment portfolio is reduced and has also tried to maximize the profit if it is withdrawn early from the particular stock. It has also been seen that public moods towards particular stocks are related with the financial markets to a greater extent.

We plan to use long short term memory networks, wherein we firstly do the user’s savings, incomes, assets, liabilities, etc. where we compare different datasets related to the stock, which helps in getting better predictions. Secondly, we compare the portfolios of different Superstars to get a better prediction. Lastly, we go through the historical data that are available and compare it, so we get predictions accurately. In this project, we aim to build a system for predicting portfolio risk using AI/ML and provide insights on how the stocks will perform. We will train our model on datasets which include historical data and predict the outcome that where user can invest Portfolio management is the practice of choosing and managing various investments, with the twin goals of maximizing returns while minimizing risk, for an entity (be it an institution, a company, or an individual investor). While some prefer to manage their own investments – especially in the era of trading apps and retail market manias – it’s very common for portfolio managers to oversee an entity’s portfolio of assets.

Generally, there are two types of portfolio management:

- Passive Management: Also known as index investing, his management style typically involves index funds or exchange-traded funds (ETFs) and is more or less a “set and forget” type of investing.

- Active Management: As the name suggests, this involves a portfolio manager actively buying and selling equities in an attempt to find alpha, an industry euphemism for outperforming the market.

A. Objective

The major goal is to ensure a specific expected return while reducing investment risk. The short- and long-term investing goals, as well as the amount and kinds of risks an investor is ready to accept, must first be determined by the investors or portfolio managers. The quantity of capital, time limits, asset classes, liquidity, geographic locations, ESG (environment, social, governance) considerations, "duration" (sensitivity to interest rate fluctuations), and currency are additional constraints.

Whether hedging FX or credit risks is allowed or not (using FX forwards and CDS), having more than 10% of cash is allowed or not, investing in developed markets is allowed or not, how much market volatility is allowed, whether investing in companies with market cap less than $1 billion is allowed, whether investing in coal or oil companies is allowed or not, whether investing in currencies is allowed or not, etc. – those are all portfolio constraints too.

- The main objective is to minimize the risk of the investment while guaranteeing a certain expected return.

- To define the short term and long-term investment goals, and how much and which types of risks the investor is willing to take.

- To select the most valuable assets to invest in.

- Algorithmic trading can be considered as a special case of price strategy.

- Mathematical and statistical techniques which solve optimization and simulation problems in investment management.

- To calculate the best accuracy of proposed system.

II. PROBLEM STATEMENT

Constructing an optimal portfolio by selecting the best possible combinations of different portfolios is a computationally challenging problem since it comes up with an exponential complexity. In this project, we aim and proposed to build a system for predicting portfolio risk using AI/ML and provide insights on how the stocks will perform.

A. Project Scope

This proposed system provides a review on machine learning methods applied to the asset management discipline. Firstly, we describe the theoretical background of both machine learning and finance that will be needed to understand the reviewed methods. Next, the main datasets and sources of data are exposed to help researchers decide which the best ones to suit their targets are. After that, the existing methods are reviewed, highlighting their contribution and significance in the analysed financial disciplines. Furthermore, we also describe the most common performance criteria that are applied to compare such methods quantitatively.

Finally, we carry out a critical analysis to discuss the current state-of-the-art and lay down a set of future research directions.

III. REQUIREMENT ANALYSIS

A. Hardware Prerequisites

- Memory (RAM): 8 Gigabytes, Facilitates smooth multitasking capabilities for concurrent server operations, database management, and user interactions.

- Storage (Hard Disk): 500 Gigabytes, Offer’s ample space to accommodate the application, user-generated data, and associated files, thereby ensuring responsive performance.

- Processor: Intel Core i3/i5, Provides efficient processing power essential for seamless application functionality.

- Display: 15-Inch Shaded Screen, Furnishes a visually clear interface conducive to comfortable user interaction.

- Input Device: Web Console Keyboard, Facilitator’s text-based inputs to enhance user engagement within the system.

B. Software Prerequisites

- Operating System: Windows & and above

- Programming Language: Python 3.8

- Tool: Visual Studio

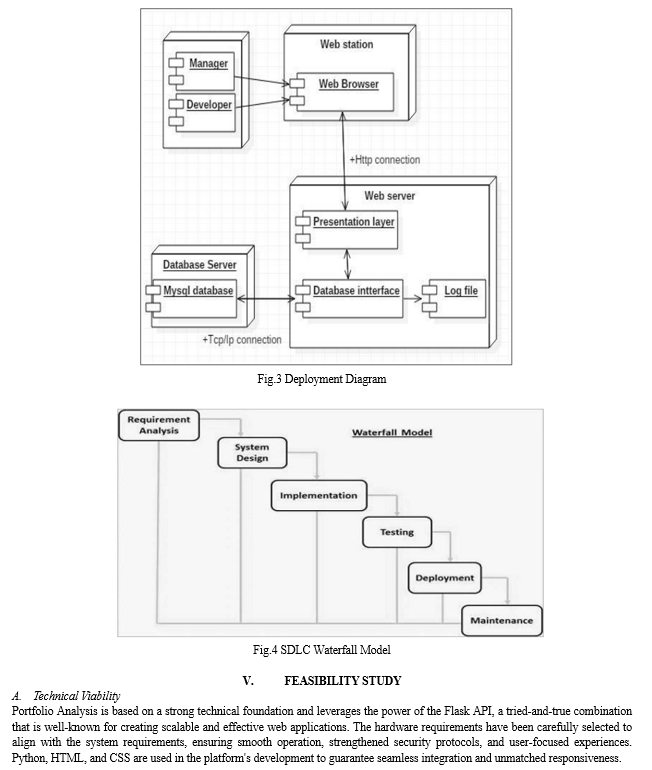

- Front End: HTML, CSS, Flask

- DBMS: MYSQL

C. System Modules

- Data Collection Module: This module is responsible for collecting and aggregating market data from various sources.

- Data Preprocessing Module: This module preprocesses the collected data, removing any missing or inconsistent data points, and preparing the data for analysis.

- Machine Learning Module: This module applies machine learning algorithms to the pre-processed data to identify patterns and make predictions on future market trends.

- Portfolio Management Module: This module manages the user’s investment portfolio, providing real-time updates on portfolio performance, and personalized recommendations on investment opportunities.

- User Interface Module: This module provides the user interface for the investment management system. The module allows users to view their portfolio performance, receive recommendations, and adjust their portfolios. The user interface is designed to be intuitive and user-friendly.

VII. ACKNOWLEDGEMENT

We would like to express our gratitude to the publishers and academics for making their resources available. We also acknowledge the college administration for providing the necessary infrastructure and assistance, as well as the guide and mentor for their insightful recommendations.

Conclusion

In this proposed system we explore the properties of machine learning factor-based portfolios. We then examine whether factor-implied covariance matrices based on machine learning dimensionality reduction techniques can benefit minimum-variance portfolios comprised of individual stocks. Overall, our findings indicate that machine learning can help improve factor-based portfolio optimization. In this project, we explored the integration of machine learning techniques into investment portfolio management. Leveraging the power of the Flask API, we developed a system that optimizes risk-adjusted returns while minimizing exposure. We created a system that maximizes risk-adjusted returns while lowering exposure by utilizing the Flask API\'s capability. Through the application of AI/ML models and historical data analysis, we illustrated the possibility of enhanced portfolio optimization. Machine learning holds great promise for improving financial decision-making as it develops further.

References

[1] Markowitz, H.M. (March 1952). \"Portfolio Selection\". The Journal of Finance. 7 (1): 77–91. doi:10.2307/2975974. JSTOR 2975974. [2] Sharpe, William F. (1964). \"Capital Asset Prices – A Theory of Market Equilibrium Under Conditions of Risk\". Journal of Finance. XIX (3): 425–442. doi:10.2307/2977928. hdl:10.1111/j.1540-6261.1964.tb02865.x. JSTOR 2977928. [3] The Valuation of Risk Assets and the Selection of Risky Investments in Stock Portfolios and Capital Budgets, John Lintner, 1965, Review of Economics and Statistics. 47:1, pp. 13–37. [4] \"Equilibrium in a Capital Asset Market\", Econometrica, 34, 1966, pp. 768–783. [5] “A fast and elitist multiobjective genetic algorithm: NSGA-IIK”, Deb, A Pratap, S Agarwal, T MeyarivanIEEE transactions on evolutionary computation 6 (2), 182-197, 2002 [6] Anagnostopoulos, K.P. & Mamanis, Georgios. (2010). A portfolio optimization model with three objectives and discrete variables. Computers & Operations Research. 37. 1285-1297. 10.1016/j.cor.2009.09.009. [7] Ye Wang, Bo Wang, Xinyang Zhang,A New Application of the Support Vector Regression on the Construction of Financial Conditions Index to CPI Prediction, Procedia Computer Science, Volume 9, 2012, Pages 1263-1272, [8] Felipe Dias Paiva, Rodrigo Tomás Nogueira Cardoso, Gustavo Peixoto Hanaoka, Wendel Moreira Duarte, Decision-making for financial trading: A fusion approach of machine learning and portfolio selection, Expert Systems with Applications, Volume 115, 2019, Pages 635-655. [9] Rapach, David & Zhou, Guofu, 2013.\"Forecasting Stock Returns,\" Handbook of Economic Forecasting, in: G. Elliott & C. Granger & A. Timmermann (ed.), Handbook of Economic Forecasting, edition 1, volume 2, chapter 0, pages 328-383. [10] RAPACH, D. E., STRAUSS, J. K., & ZHOU, G. (2013). International Stock Return Predictability: What Is the Role of the United States? The Journal of Finance, 68(4), 1633–1662. [11] Harvey, Campbell R. and Liu, Yan, Detecting Repeatable Performance (January 21, 2018). [12] Li Bin, SHAO Xinyue, LI Yueyang. Research on fundamental quantitative investment driven by machine learning [J]. China Industrial Economics,2019(08):61-79. [13] Jigar Patel, Sahil Shah, Priyank Thakkar, K Kotecha, predicting stock market index using fusion of machine learning techniques, Expert Systems with Applications, Volume 42, Issue 4,2015, Pages 2162-2172.

Copyright

Copyright © 2024 Payal Narale, Vinay Lachotra, Krushna Nalawade, Sakshi Karanje, Savita Vibhute. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET59541

Publish Date : 2024-03-28

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online