Ijraset Journal For Research in Applied Science and Engineering Technology

Role of Microfinance on Women Empowerment in Siddharth District of U.P

Authors: Shiv Kumar Maurya, Professor Deepak Babu

DOI Link: https://doi.org/10.22214/ijraset.2023.56447

Certificate: View Certificate

Abstract

A large portion of the population currently lives below the poverty line (BPL), which is a problem for emerging nations. Microfinance can aid developing nations in overcoming their poverty issues. Micro-finance offers a variety of financial resources (such as loans, insurance, savings, etc.) to the underprivileged so they can stabilize their businesses. Individuals can use these resources for a wide range of purposes, including pursuing business possibilities, raising their standard of living, paying off other sizable debts, responding to emergencies, etc. Microfinance is the arrangement of financial services including loans, savings, insurance, money transfers and remittances offered to the lower income groups or poor entrepreneurs, who otherwise cannot avail the standard banking services. The motive behind Microfinance is to give people in poverty a privilege to become self-sufficient by offering them crucial banking services at considerable smaller monetary amounts.

Introduction

I. INTRODUCTION

Once seen as a tool for women’s empowerment, microfinance is now recognized as a critical component of the fight against poverty. Mohammed Yunus, a Noble Prize winner, and a few volunteers started a crucial experiment in Bangladesh. Mohammad Yunus believed that giving credit to the poor was important for their stability and financial needs, but it was also important for them to raise their level of living by giving them access to the resources they needed. He began offering small loans to groups of borrowers, primarily women, who wanted to launch their own businesses with no collateral or little collateral. His work expanded and became the movement’s primary building block, which greatly aided microfinance in expanding. At the beginning, microfinance simply offered unsecured loans, but today there are many different services like payments, insurance, savings, money transfers, etc. available. The number of families with access to microcredit, which currently numbers 70 million of the world’s poorest families, is increasing by more than 35% annually.

The National Bank for Agricultural and Rural Development (NABARD) launched the microfinance programme in 1992. It is currently the biggest microfinance programme in the world. The Indian microfinance programme began and grew in the Southern area, and only subsequently, primarily in 2005 and beyond, did it spread to other regions. Self-Help Groups (SHGs) and Microfinance Institutions are the main sources of microfinance in India (MFIs). The network of many financial institutions, including commercial banks, cooperative banks, regional rural banks (RRBs), and microfinance organizations, is available to the needy in rural areas (MFIs). These banks offer a variety of loan options for small businesses in need of working capital, as well as larger loans for durable items, loans for children’s education, and loans for unexpected expenses.

A small, voluntary organization of these low-income individuals, ideally from a similar socioeconomic background, is known as a self-help group (SHG). People come together to work through their shared issues in self-help groups and with one another. The SHGs encourages members of the group to save small amounts in a designated bank. This joint account is held in the SHG’s name. A significant portion of the population in India relies on unofficial sources of credit, such as small businesses, families, friends, and moneylenders, who, despite their drawbacks, are nevertheless favored. Their restricted use of the established banking system is the cause. Self Help Group-Bank Linkage Program is the name of the strategy created to give this low-income group of unbanked people access to formal sources of funding (SBLP). Under this concept, any NGOs, also known as Self Help Promoting Institutions, organize SHGs of 10 to 20 people (SHPIs). The SHGs also engage in livelihood activities for which specific NGOs or universities offer skill training. The SHG members are encouraged to save money and lend it to other members when they need it. Additionally, SHPIs are taught how to manage the relevant books of accounts.

Only 33% of Micro-finance clients are men, and 67% of the total clientele are women, making up the majority of the industry. Small and marginal farmers, agricultural workers, artisans, craftspeople, and other low-income individuals who operate small businesses, such as carpentry, transportation, vegetable sales, boutiques, beauty salons, dairy and fisheries, animal husbandry, pickle and papad production, sewing, and more, make up these clients.

The primary goals of the Twelfth Five Year Plan were to promote inclusive growth and the eradication of poverty. Without micro-finance, it will be challenging for the poor to escape the cycle of poverty. Micro-finance can significantly help the poor become financially included. The Self Help Group-Bank Linkage Program (SBPL), Microfinance Institutions, Cooperative Banks, State Financial Corporations, Regional Rural Banks, and Primary Agricultural Credit Societies are just a few of the channels that can help the poor get credit. All of these channels need to be strengthened.

II. FUNCTIONS OF MICROFINANCE

- Financial Assistance: Micro-finance offers low-income people financial support so they can cope with life’s inevitable events, such as marriage, death, and education.

- Improve the Capacity to Handle: Microfinance increases a person’s ability to handle catastrophes like personal crises and natural disasters, which lowers their vulnerability.

- Microfinance offers chances to invest in companies, properties, or other household goods.

- The microfinance programme can aid in lowering issues with poverty and economic inequality.

- The socioeconomic growth of the rural area and its inhabitants is facilitated by microfinance.

- Quick Loan Disbursement: Micro-finance loans are disbursed quickly and with few requirements. Microfinance offers additional income-generating opportunities and aids in a person’s economic independence.

Hence, the term “micro-finance” refers to limited loan, insurance, and savings services offered to socially and economically underprivileged groups in society. Micro-finance has developed as a method of economic development aimed at helping low-income groups in rural areas. Micro-finance is the word used to describe the supply of financial services, including income-generating activities, to low-income groups. Credit and savings are two common financial services, but some self-help organisations that fall under the umbrella of microfinance also offer insurance services. Also, a lot of MFIs offer social services such group creation, character building, training for financial literacy, and the development of managerial skills among group members. In addition to credit and savings options, microfinance has evolved to become one of the main drivers of growth in rural communities.

III. WOMEN EMPOWERMENT

The term "Women's Empowerment" (or "Female Empowerment") can be used to describe a variety of actions, such as valuing women's opinions or making an effort to find them, as well as elevating women's position through knowledge, awareness, literacy, and training. Women's empowerment gives them the tools and freedom to choose how to live their lives in response to societal issues. They might be given the chance to redefine gender roles or other kinds of roles, which would provide them more freedom to accomplish their objectives.

IV. SELF-HELP GROUPS (SHG)

A group of people who gather together to solve a similar financial issue is referred to as a self-help group, according to NABARD, a self-help group is made up of 10 to 20 low-income individuals who meet together to tackle a similar financial issue. Members voluntarily make daily, weekly, or monthly contributions to a communal fund in order to mobilize their savings and meet their finance needs. The Self-Help Group is a self-governed, peer-controlled small and informal organization of the impoverished people, adhering to the same homogeneous families, according to the Indian Planning Commission (NITI Aayog). SHG members get together once a week or once a month to discuss and try to solve their shared issues. With mutual assistance, it enables the group members to transform their financial and social problems.

V. SIDDHARTH DISTRICT: AREA OF THE STUDY

The district is located between latitudes 270 and 27028’N and longitudes 82045’E and 83010’E. On the north, the district is bordered by Nepal; on the east, Maharajganj; on the south, Basti and Sant Kabir Nagar; and on the west, Balrampur. On December 29, 1988, the Basti district was divided, creating the district. As Prince Siddharth, the Buddha’s pre-enlightenment name, spent his early years (up until the age of 29) in Kapilvastu, which is located within the boundaries of this district, the district was given his name.

VI. RESEARCH METHODOLOGY

A. Objective Of The Study

To study the role and importance of Microfinance Services on Women Empowerment in District Siddharth Nagar of U.P.

B. Methodology

The present study is based on primary as well as secondary data. The primary data was collected by using the questionnaire survey amongst the participant members of the micro finance program. Participants are the member of SHGs, who have been benefited from the Micro-finance schemes and received the loan.

C. Research Base

This study gave a major impetus on both the research approaches i.e. quantity and quality research by utilising ‘Questionnaire Survey Approach’ for finding the necessary and the relevant facts and collecting data. The research methodology comprised of questionnaire survey of questions which were being asked to the target Group. The method adopted was that the researcher collected the database of the SHGs from Micro-finance credit agencies. Further, from these groups, the respondents who availed the credit facilities and completed two years were selected.

D. Data Collection

The two sources are used for data collection, i.e., primary as well as secondary sources. Secondary data aided to provide a framework and insight based on earlier studies on the information on Micro-finance. The secondary data was collected from the various articles, journals, annual reports of NABARDA, Banks, NGOs, MFIs, etc.

The primary data gave information to the researcher on base analysis of the research, development and problem related to information needs of SHGs members in research area which was selected. The data collection technique included questionnaire surveys.

Primary data was collected from the respondents consisting of Micro-finance beneficiaries. The study area was divided into three blocks of Siddharth Nagar.

- Nauagrh

- Bansi

- Jogia

E. Research Instruments

Well structured questionnaire for the Micro-finance beneficiaries was prepared. In this study, the closed ended questionnaire was used in the collection of data.

F. Sampling Plan

Sample Size: Sample Size is 150 consisting of Micro-finance beneficiaries. Micro-finance beneficiaries are the member of SHGs, who have been benefited from the Micro-finance schemes and had received the bank loan.

Conclusion

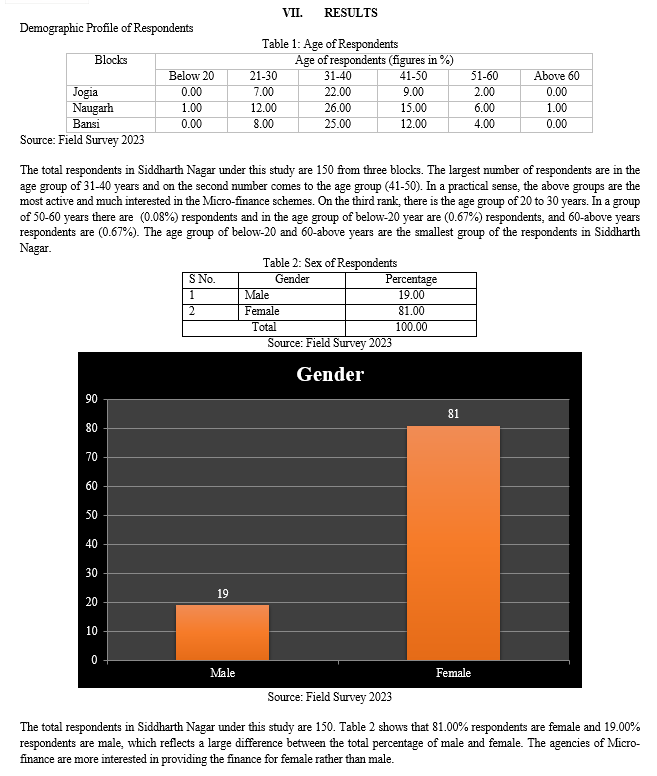

This study shows that the demographic profile indicates that maximum respondents in Siddharth Nagar belonged to the age group of 30-40 and . It can be further concluded that agencies of Micro-finance are more interested in providing finance for females rather than males. The age group of below-20 and 60-above years are the smallest group of the respondents in Siddharth Nagar. The data reveals very high participation of Hindus in SHG program followed by the very low participation of Muslims in Siddharth Nagar when respondents were analysed with religion as a demographic factor. The percentage of illiteracy was found high among all 3 block of Siddharth Nagar. Among literates also, maximum respondents were considered to be educated up to higher secondary and high school in decreasing level. The living standards of respondents(women) saw a significant improvement from past. The women are improving themselves after getting Microfinance and their economic and social conditions have also improved after getting financial services.

References

[1] Abdullah, C., Mamun, A., Hasan, N., & Rana, A. (2013). Micro-Credit and Poverty Alleviation?: The Case Of Bangladesh, 3(1), 102–108. [2] Agbola, F. W., Acupan, A., & Mahmood, A. (2017). Does Microfinance Reduce Poverty? New Evidence From Northeastern Mindanao, The Philippines. Journal Of Rural Studies, 50, 159–171. Https://Doi.Org/10.1016/J.Jrurstud.2016.11.005 [3] Aggarwal, M., & City, J. (2014). Abhinav National Monthly Refereed Journal Of Research In Abhinav National Monthly Refereed Journal Of Research In, 3(5), 70– 73. Retrieved From Http://Abhinavjournal.Com/Journal/Index.Php/Issn-2277-1182/Article/View/195/Pdf_13 [4] Ashok K. Pokhriyal, Uniyal, J., & Rani, R. (2013). Journal Of Business And Finance, 01(01), 27–37. Https://Doi.Org/10.1177/1050651909333141 [5] Awasthi, P. B. D. (N.D.). Abstract Of Ph. D. Thesis On Role Of Microfinance In Rural Development Of Uttarakhand (With Special Reference To Almora District) Supervisor?: Uttarakhand Researcher Gaurav Pant. [6] Bakhtiari, S. (2006). Microfinance And Poverty Reduction?: International Business & Economics Research Journal, 5(12), 65–71. [7] Bambuwala, S., & Shukla, D. S. (2017). Financial Inclusion In Rural Gujarat: A Review. Iosr Journal Of Humanities And Social Science, 22(07), 06–09. Https://Doi.Org/10.9790/0837-2207010609 [8] Bandyopadhyay, S. (N.D.). Microfinance In The Improvement Of Living Standard And Gnh, 248–271. [9] Banerjee, A., Duflo, E., Glennerster, R., & Kinnan, C. (2015). The Miracle Of [10] Microfinance? Evidence From A Randomized Evaluation †. American Economic Journal: Applied Economics, 7(1), 22–53. Https://Doi.Org/10.1257/App.20130533 [11] Batinge, B. K. (2014). An Assessment Of The Impact Of Microfinance On The Rural Women In North Ghana, 30(June), 2011. [12] Beenish Ameer, & Moazzam Jamil. (2013). Effectiveness Of Microfinance Loans In Pakistan. Global Journal Of Management And Business Research, 13(7), 1–5. [13] Bhattacharyay, M. (2007). Enhancing Inclusiveness Of The Indian Financial Sector - The Role Of Microfinance. Journal Of Economic Literature, (May 2007), 1–33. [14] Bhuiya, M. M. M., Khanam, R., Rahman, M. M., & Nghiem, H. S. (2013). Impact of Microfinance On Household Income And Consumption In Bangladesh: Empirical Evidence From A Quasi-Experimental Survey. Journal Of Chemical Information And Modeling, 53(9), 1689–1699. Https://Doi.Org/10.1017/Cbo9781107415324.004 [15] Boateng, G. O., Polytechnic, T., Boateng, A. A., Polytechnic, C. C., & Bampoe, H. S. (2015). Microfinance And Poverty Reduction In, 6(1), 99–108. [16] Bushra, M. (2016). Micro Finance?: An Extension Of Banking Support To Uplift Poverty In India, 4(6), 1–10. [17] Carreras, G., & Jose, F. (2012). Does Microfinance Have An Impact? Three Quantitative Approaches In Rural Areas Of Bangladesh And Andhra Pradesh, India. Retrieved From Http://Sro.Sussex.Ac.Uk/43098/ [18] Census India. (2011). Rural-Urban Distribution, 1, 1–2. Retrieved From Http://Censusindia.Gov.In/2011-Prov-Results/Paper2/Data_Files/Orissa/4-Ex-Summery--7-8.Pdf [19] Change, A. (2014). The Role Of Microfinance In Contemporary Rural Development Finance Policy And Practice?: Imposing Neoliberalism ... The Role Of Microfinance In Contemporary Rural Development Finance Policy And Practice?: Imposing Neoliberalism As „ Best Practice ,? 12(November), 587–600. Https://Doi.Org/10.1111/J.1471-0366.2012.00376.X [20] Charles, A, & Hamed, B. (2011). Impact Of Microfinance On Poverty Alleviation In Nigeria?: An Empirical Investigation. European Journal Of Humanities And Social Science, 2(1), 97–111. [21] Cherotich, K. L. (2015). Effect Of Microfinance Services On Poverty Alleviation In, (October).

Copyright

Copyright © 2023 Shiv Kumar Maurya, Dr. Deepak Babu. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET56447

Publish Date : 2023-11-01

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online